Navigating the New York City real estate market is no small feat. From soaring prices to competitive bidding wars, finding an affordable path to homeownership can feel nearly impossible. That’s where an FHA loan NYC steps in as a practical, flexible, and achievable solution for first-time buyers and beyond.

FHA loans offer a way to break into the market without needing a perfect credit score or a 20% down payment—two major hurdles for NYC buyers. In this article, we’ll break down exactly what FHA loans are, where they came from, who qualifies, whether they can be used for land, and which types are assumable.

Let’s dive in.

What Is an FHA Loan?

An FHA loan is a government-backed mortgage insured by the Federal Housing Administration. These loans are designed to make homeownership more accessible, especially for people who may not qualify for conventional loans due to lower credit scores or limited down payments.

Key benefits include:

- Down payments as low as 3.5%

- More lenient credit requirements

- Lower closing costs

- Flexible income guidelines

For NYC residents facing some of the highest housing costs in the country, these features make an FHA loan NYC a popular and strategic option. It’s a way to gain a foothold in a market where the median home price is often out of reach with conventional financing.

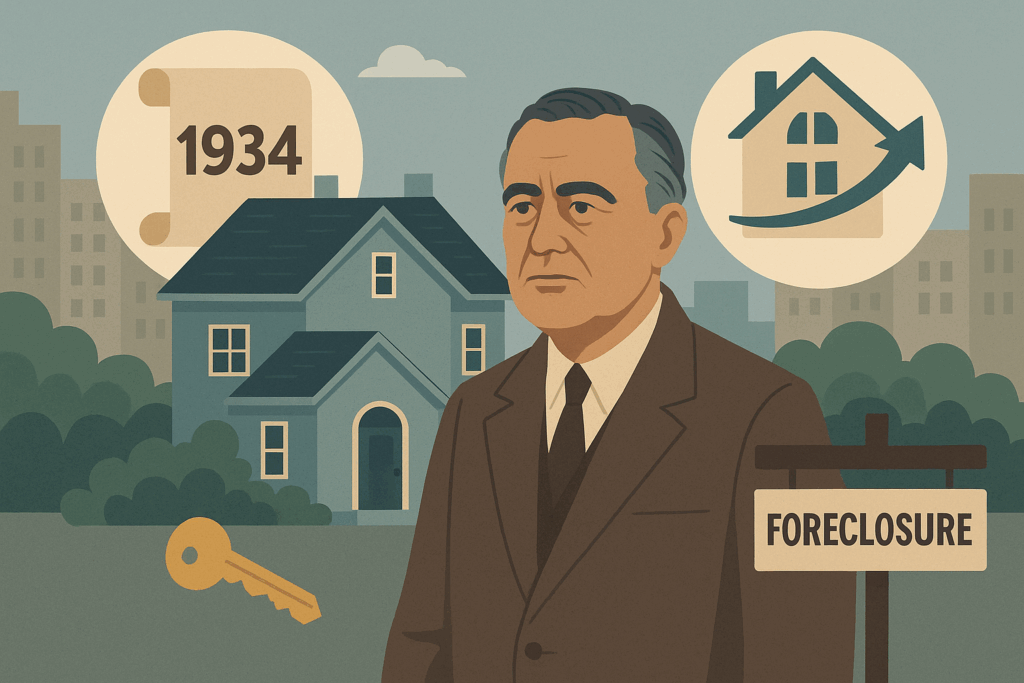

When Did FHA Loans Start?

FHA loans were introduced in 1934 during the Great Depression as part of President Franklin D. Roosevelt’s New Deal. The goal was to help stabilize the housing market by making mortgages more accessible and preventing foreclosure.

Before FHA loans, homebuyers needed up to 50% down and faced short-term balloon mortgages. The FHA fundamentally changed that model by:

- Introducing longer loan terms (up to 30 years)

- Making homeownership possible for middle- and working-class Americans

- Providing insurance to lenders in case of borrower default

This system remains the foundation of FHA loan NYC programs today, with the added benefit of helping first-time buyers navigate modern challenges like student debt, rising rents, and inflated property values.

Why FHA Loans Are Good (Especially in NYC)

Here’s why choosing an FHA loan NYC can be a game-changer:

- Affordability: Lower down payments mean you don’t need to spend years saving to buy.

- Credit Flexibility: Borrowers with credit scores as low as 580 can qualify for 3.5% down.

- High Cost Limits: NYC’s high property values are considered, with loan limits up to $1,149,825 in certain boroughs.

- Support for First-Time Buyers: Paired with down payment assistance programs in NYC, FHA loans help new buyers enter the market.

- Assumability: We’ll explain later how this feature can benefit both buyers and sellers in a high-rate environment.

Follow Starr Mortgage Company on LinkedIn and Facebook to stay updated on loan options and rate changes relevant to your area.

Who Offers FHA Loans?

FHA loans in NYC are offered by approved private lenders—not directly by the federal government. These lenders must meet strict guidelines set by the Department of Housing and Urban Development (HUD).

At Starr Mortgage Company, we are proud to be an approved FHA lender with decades of experience helping New Yorkers navigate their loan options. Whether you’re buying a co-op in Queens or a duplex in Brooklyn, our team understands the nuances of the local market and the FHA guidelines that support your goals.

Have questions? Contact us at 845-348-3172 or [email protected].

Can You Use an FHA Loan for Land?

This is a common question—and a nuanced one.

FHA loans are not intended for raw land purchases. They are specifically designed to finance primary residences, which means there must be a home on the property that meets HUD’s minimum standards.

However, there is one exception:

FHA construction-to-permanent loans allow you to purchase land and build a home, all in one package—if you meet certain criteria.

These loans are more complex, require additional documentation, and are not offered by every lender. But for the right buyer with a specific vision, it may be possible to build your dream home using an FHA loan NYC, even if it starts with purchasing land.

Follow Starr Mortgage on X (formerly Twitter) to stay up to date on changing loan programs and guidelines that impact land purchases and construction loans.

Which FHA Loans Are Assumable?

One of the most underrated features of an FHA loan in NYC is assumability.

Here’s what that means: If you buy a home with an FHA loan, the next buyer can “assume” your loan—taking over your interest rate, monthly payment, and balance—rather than securing a new mortgage.

This is a powerful tool in a rising interest rate environment. Imagine locking in a 3.25% rate today and selling in five years when rates are 6%. Your loan becomes a huge selling point.

Not all FHA loans are assumable, but most fixed-rate FHA loans are—provided the new borrower qualifies. If you’re looking at long-term investment or resale potential in NYC’s shifting market, this feature adds real value.

Want to know if assumability works in your situation? Contact us for a free consultation.

Make Homeownership in NYC a Reality

Whether you’re dreaming of a brownstone in Harlem, a condo in Astoria, or a family home in Staten Island, an FHA loan in NYC could be the key to unlocking that door. With lower down payments, flexible credit requirements, and the ability to assume favorable rates, FHA loans are designed to open up opportunities in even the toughest markets.

Still have questions? Our team at Starr Mortgage Company is here to walk you through every step of the process—from pre-qualification to closing and beyond.

Start your homeownership journey today with Starr Mortgage Company.

Call us at 845-348-3172

Email us at [email protected]

Schedule a free consultation

Want to explore what others are saying? Read reviews on Yelp or follow us on Facebook, LinkedIn, and X for insights, updates, and tips on smart borrowing in NYC.

Let’s make your New York dream a reality—with the right loan and the right team.